Stay compliant and protect your business with this in-depth guide to annual report filing. Learn key requirements, deadlines, and how securing documents like a certificate of good standing or certificate of existence ensures your company remains in good standing. Plus, explore how third-party experts like CSC can streamline multi-state filings and compliance management.

An annual report in USA is a mandatory filing required by most US states for LLCs and corporations. It confirms that the company is still active and updates key business and ownership details with the state authority.

This report generally includes company information such as registered office address, registered agent details, management or member information, and in some cases, basic financial statements in USA. Filing the annual report on time is essential to maintain good standing and avoid penalties or administrative dissolution.

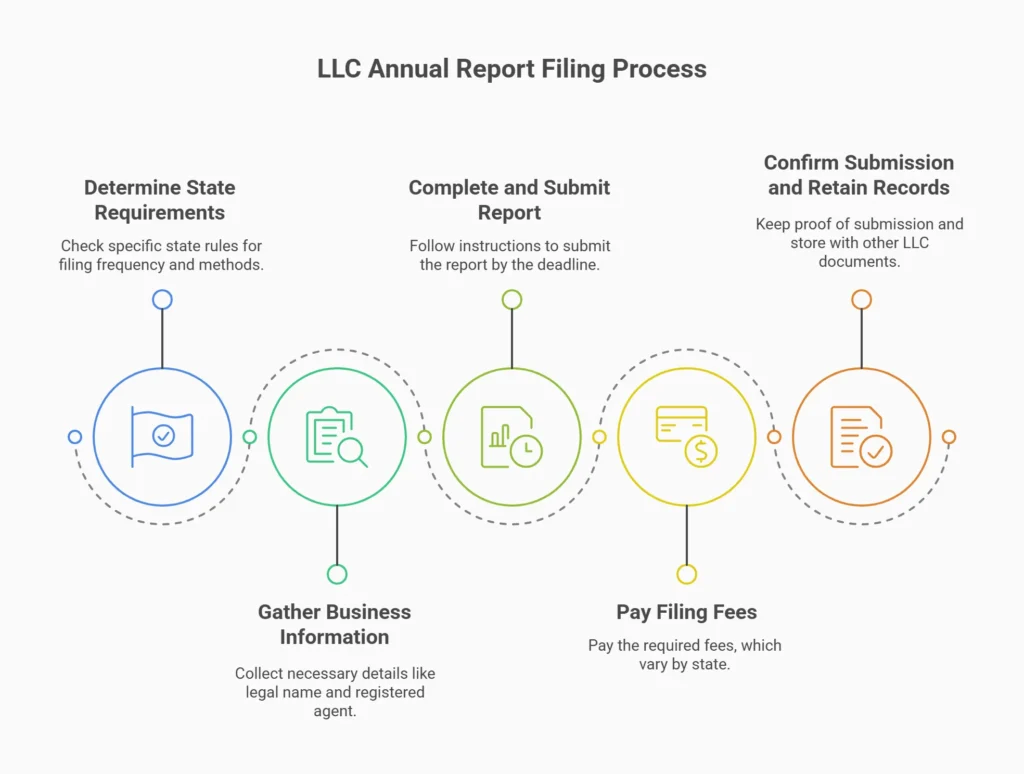

The filing deadline for the annual report in USA depends on the state where the company is registered. Each state follows its own timeline and rules.

Some states require annual reports to be filed by a fixed calendar date, while others link the deadline to the company’s formation anniversary. A few states allow biennial filings instead of annual ones.

It is important to track state-specific deadlines, as missing the due date can result in penalties or compliance issues. Filing early helps avoid last-minute errors and ensures uninterrupted business status.

The purpose of an annual report is to provide transparency, foster stakeholder trust, and comply with regulatory requirements. Filing an annual report ensures that a business remains compliant with state laws, avoids penalties, and retains its good standing status. Non-compliance can result in fines, dissolution, or loss of legal protection.

There are two main types:

Compliance-focused annual reports (submitted to state agencies)

These reports and requests often involve the retrieval of a certificate of good standing or certificate of existence.

Shareholder-focused annual reports (financial reports for stakeholders)

These regulatory documents verify certificate status and their public availability ensures transparency.

Good standing refers to a business maintaining compliance with state laws, allowing it to legally operate, enter contracts, and maintain liability protections. Filing an annual report fulfills legal obligations and acts as a verification tool, demonstrating certificate status, confirming that an entity is active and conducting business legally.

A business in good standing can secure financing, enter contracts, and maintain partnerships without interruptions caused by compliance issues. Entities not in good standing may lose the right to initiate or defend lawsuits in some jurisdictions. Good standing is often a prerequisite for renewing professional licenses or permits required for business operations.

For LLCs and corporations, failing to file can lead to the loss of limited liability protections, exposing owners to personal liability. Losing good standing in one jurisdiction can affect the ability to operate in others, particularly for entities requiring foreign qualification. Being listed as “inactive” or “not in good standing” in public records can damage trust with customers, investors, and partners. Non-compliance with annual report requirements can lead to the automatic dissolution of the entity, requiring costly and time-consuming reinstatement.

Understanding the requirements for annual reports is essential to ensure compliance, maintain good standing, and effectively communicate with stakeholders. These requirements vary widely based on the jurisdiction, industry, and type of organization, but some common elements form the foundation of most reports. Failing to meet these requirements can result in penalties, business dissolution, or the inability to obtain key compliance documents, such as a certificate of good standing, certificate of authorization, or a certificate of existence.

Most registered business entities, including domestic and foreign entities operating within a jurisdiction, are required to file annual reports. These entities include:

LLCs: Typically need to provide member or manager information.

Corporations: Required to report on officers and directors.

Limited partnerships (LPs) and limited liability partnerships (LLPs): Often need to file, depending on the state, and may require additional certificates verifying their legal status.

Non-profits: Filing requirements vary, with some states offering exemptions or simplified processes. Sole proprietorships and unincorporated businesses are generally exempt, as they do not register at the state level.

The deadline for filing an annual report varies by jurisdiction and entity type. Public companies in the U.S., for example, must file their annual reports (Form 10-K) with the U.S. Treasury Securities and Exchange Commission (SEC) within 60 to 90 days after the end of their fiscal year, depending on their size. Private companies and non-profits often have more flexible deadlines but should confirm specific filing requirements with their local regulatory authority. Missing a filing deadline can result in late fees, loss of good standing, and difficulties obtaining a certificate of existence for business transactions.

Filing frequency depends on the jurisdiction:

Annual filing: Many states require entities to file reports every year to remain in good standing and continue business operations without disruption. These filings often require accompanying certificates to verify an ongoing compliance status and entity existence.

Biennial filing: Some states, such as Iowa and Indiana, require reports every two years. Businesses should verify their state’s requirements to avoid lapses in compliance that could impact their ability to obtain a certificate of good standing.

Meeting the deadline for filing an annual report is a critical aspect of maintaining a business’s legal compliance and good standing. Missing an annual report filing deadline can lead to several negative consequences, both financial and operational, that businesses must proactively avoid.

No matter how many entities you have and where they are registered, we make it easy to hand off management of your annual reports to us.